How the Economic Machine Works by Ray Dalio

Interactive Graph

Table of Contents

This is going to be my written understanding of Ray Dalio’s absolutely beautiful 30 minute animated video to answer the question, “Hoe does the economy really work?” To any reader, watch the original video first. It’s one of the best presented educational videos on the internet in my opinion.

The Machine Template

Ray describes the economy as a simple machine, a machine that many people don’t understand or agree upon. He claims he as a simple but practical economical template that paints an accurate picture of the economy and markets in a country, which allowed him to sidestep the global financial crisis and has worked well for him for the last 30 years.

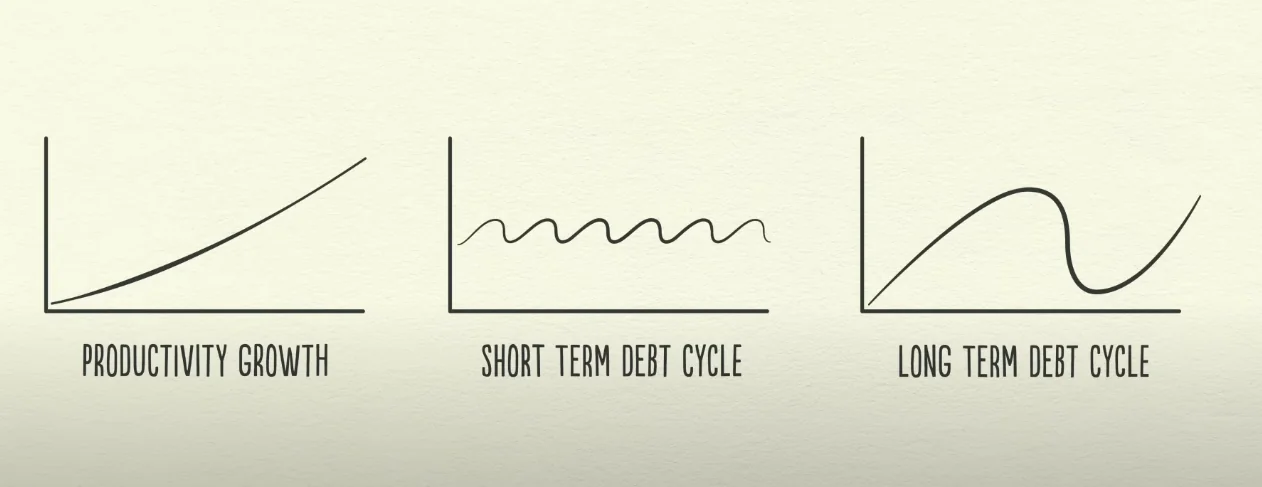

Forces That Drive the Economy

According to Ray, there are three primary forces that drive the economy. Productivity growth, the short-term debt cycle and the long-term debt cycle .

His template, focuses on only layering these three forces together, and observing the effect it has on transactions and how that in turn affects the economy.

Transactions

To start modelling the economy, we should first understand what we’re talking about when we say the word ’economy.'

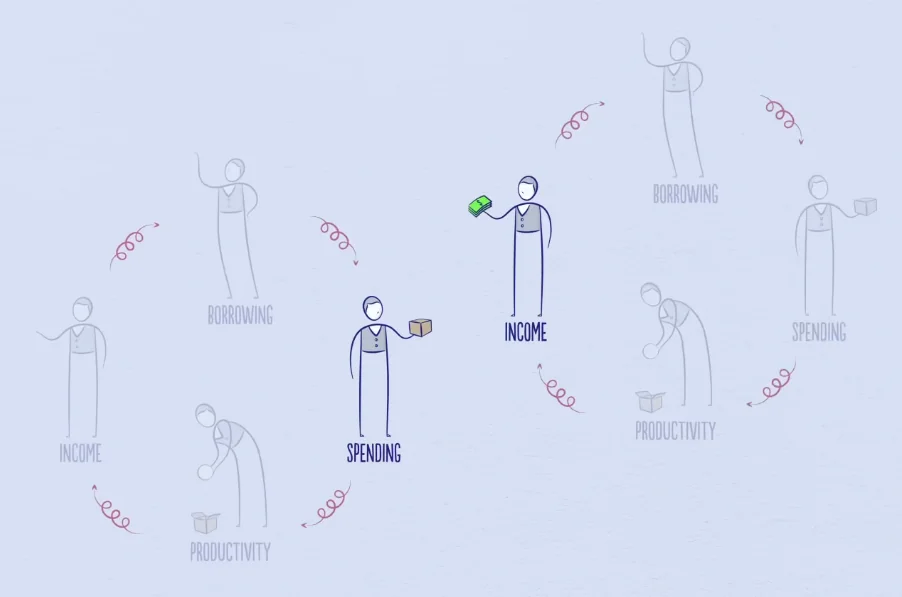

An economy is simply the sum of the transactions that make it up, and a transaction is a very simple thing. Everyone makes transactions all the time. Every time you “buy” something, you create a transaction. Each transaction consists of a buyer exchanging money or credit, for goods, services, or financial assets.

Spending credit, is the same as spending money. So simply summing up the amount of credit spent and money spent, we can calculate the total spending of a nation. And the total amount of spending drives the economy. Let the total spending in a country be $T$. If $T_m$ is the total money spent, and $T_c$ is the total credit spent, we have $T = T_m + T_c$. Now, let the total weighted-quantity sold be $Q$. Now the price of $Q$ is just $P = \frac{T}{Q}$. Keep this in mind for later, it’ll help reason about why prices increase during an inflation and decrease during a deflation. So if a buyer, pays price $P$ to buy some item / service $Q$, we have a transaction.

Transactions are the basic building block of the economic machine described by Ray. All cycles and forces in an economy are driven by transactions. Understanding transactions will help us understand the entire structure and working of the economic machine.

Market

A market consists of all the buyers and sellers making transactions for the same thing. For example, we have a wheat market, a stock market, a car market, etc.

Economy

An economy consists of all of the transactions in all of its markets. If you add up the total spending and the total quantity sold in all of the markets, we have everything we need to know to understand the economy.

The Participants

The participants involved in transactions are people, businesses, banks & governments.

The Government

The most important buyer and seller that we want to understand is the government. It is primarily the actions of the government that control inflation, deflation, and all the other large scale economic events that occur. The government consists of two parts:

- CENTRAL GOVERNMENT The central government is the body responsible for collecting taxes and interacting with the people. This is important because they collect taxes from the people, usually proportional to wealth and redistribute it back to the have-not in difficult times via stimulus checks and other similar means of support.

- CENTRAL BANK It is different from other buyers and sellers because it controls the amount of money and credit in the economy. The central bank is both capable of influencing interest rates and printing new money. The central bank is an important player, perhaps the most important player in the flow of credit in the economy.

People & Businesses

Both work roughly the same way. Both people and businesses use the capital and income available to them to buy assets and other items by partaking in transactions. In particular, they act as propagators in the economic machine. People and businesses often take up debt, giving them access to credit to increase their spending. This will be covered in detail soon.

Banks

Similar to the described central bank above. They cannot print money, but they can adjust the interest rate and thereby help control the flow of credit in the economy.

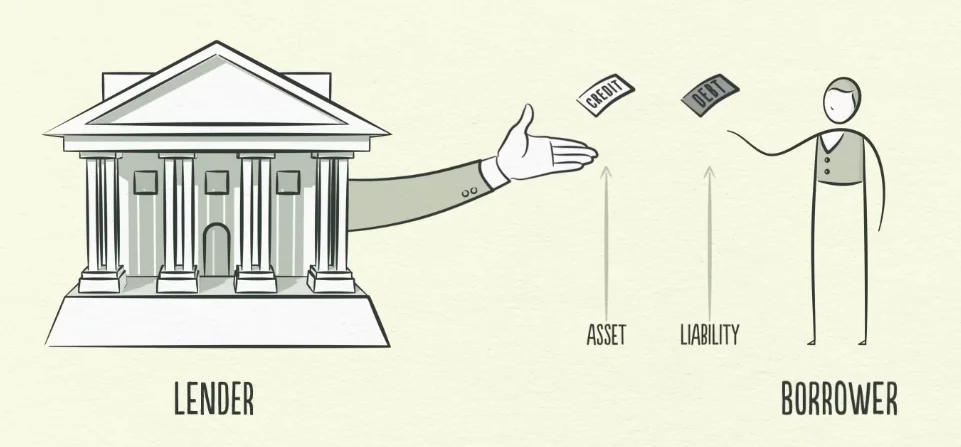

Credit

Is is THE most important part of the economy and often the least understood. It is important because it’s extremely volatile and because a huge proportion of transactions that happen are done with credit. In 2021, the national debt of India amounted to around $2.36$ trillion USD while the money in circulation in 2021 is only 0.341 trillion USD.

How Is Credit Created?

Out of thin air actually. Just like buyers and sellers make transactions in a market, so do lenders and borrowers. (Slight misconception involved here, will be cleared in the “MISCONCEPTIONS” section).

Lender and Borrower Dynamic

Lender Incentive

Lender’s want to make their money work for them and generate more profits. So they often give loans to borrowers who agree to pay back the loan with some interest over a period of time. Essentially, they give money to a borrower on an agreement that the borrower will return them the principal amount along with some extra interest within some period of time. This assures them profits as long as the borrower doesn’t go bankrupt and default on the loan.

Borrower Incentive

This depends. It is possible the borrower might want to buy something that they can’t outright afford, like a new car or house. Or maybe they want it as an investment into funding a new business they might want to start. The credit (loan) allows them to stretch a big investment over a period of time (EMI (Equated Monthly Installment) for example) or in funding their risky business idea that might generate them profits, using which they can pay back the loan and still have made more profit than incurred losses in interest payback. You can also think of it this way, for an individual that used his credit to take his loan, he uses credit to smoothen his buying power over time. He knows he’ll have more buying power in the future as his income will increase, so he wants to increase his buying power now itself, and not have it be a direct function of his exact current income.

Essentially, this lending and borrowing of money agreement allows both borrowers and lenders to get what they want. When such an agreement is made, credit is created. However, there are some important factors that control credit creation.

Factors That Influence This Dynamic

Interest Rate

As mentioned previously, borrowers pay back the principal borrowed along with some extra interest. This is typically simple or compound interest. In either case, the extra amount repaid depends on a number called the interest rate. When interest rates are high, there is less borrowing because it’s expensive. But when interest rates are low, borrowing increases because it’s cheaper.

Creditworthy Score

The risk associated with making money for the lender comes from whether or not they believe the borrower to be able to pay back the principal in worst-case situations. For example, a lender would probably not reach this agreement with someone who wants to gamble all the borrowed money in a casino. Usually, borrowers have some private financial assets they can put down as collateral for the loan. In case they go bankrupt, the lender can rely on the borrower to sell the asset and repay the borrower with that money. However, keep in mind that this is still not completely safe, as the price of financial assets can go up or down depending on the demand and supply for that asset. However, income and collateral are still widely used to judge the creditworthy-ness of individuals to decide how much credit can be trusted to them.

When any two people engage in this agreement, with a borrower promising to repay and a lender who believes in the borrowers and gives him the money, credit is created. Yes, out of thin air.

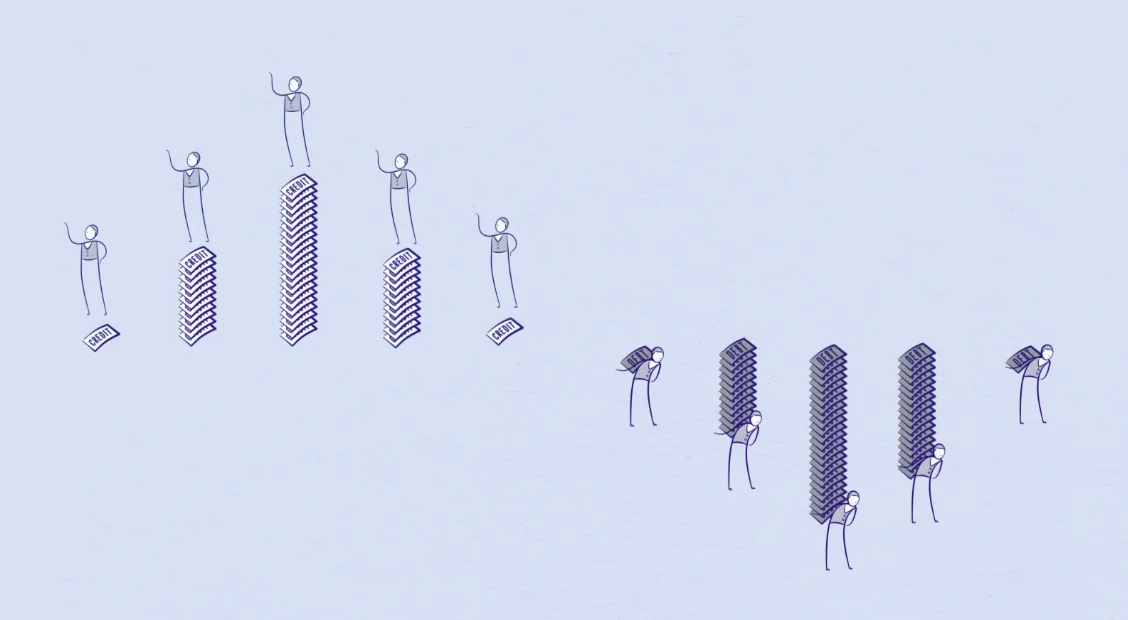

Debt

Credit goes by many names. Debt is like the twin-brother of credit. As soon as credit is created, so is debt. Let’s say a lender $A$ loans Rs. $x$ to a borrower $B$. Immediately, credit and debt are created. The lender receives a credit asset of value Rs. $x$ + $I$ , where $I$ is the interest to be paid, and the borrower receives a debt liability of value Rs. $x+I$.

How Is Credit Destroyed?

In the future, when the borrower repays the loan, plus the interest amount, he completes the transaction and both the asset (credit) and liability (debt) associated with that loan disappear.

Common Misconceptions

The word credit is often used to describe many different things. In the context of this template, we will use the term credit to describe two things:

- AN ASSET - Here, we mean credit as essentially a bookkeeping entry for the lender that he expected to make some $x + I$ amount by a future date.

- EXTRA CAPITAL - Credit can also refer to the ’extra’ borrowed money that the borrower now has access to. This is mostly what we’ll be referring to when we use the word credit in the future. This is important, because this is a major driving force of economic growth. Essentially, think of it this way, no new money is actually created, but the amount of money involved in transactions is now greater. Why? The money given by the lender is money that the lender would’ve otherwise just let lie dormant as cash. However, because he sees a net positive ROI on lending the money to the borrower, he gives away this money and then this money is injected into the economy via the borrower who uses this extra capital to make transactions. This extra capital is just money that the borrower borrows from his future self. However, by borrowing money and making transactions with it, he essentially allows this ’extra’ money which would’ve not partaken in transactions to now help increase the expenditure in the economy at the present.

The Operation of the Machine

You can probably figure out everything from scratch as long as you keep in mind this single mantra, that pretty much dictates all the why’s in the operation of this machine.

One person’s spending is another person’s income. Every dollar you spend, someone else earns. And every dollar you earn, someone else has spent. So when you spend more, someone else earns more. When someone’s income rises, it makes lenders more willing to lend him money because now he’s more worthy of credit. … So increased income allows increased borrowing, which allows increased spending. And since one person’s spending is another person’s income, this leads to more increased borrowing and so on. (Remember, the opposite also holds true).

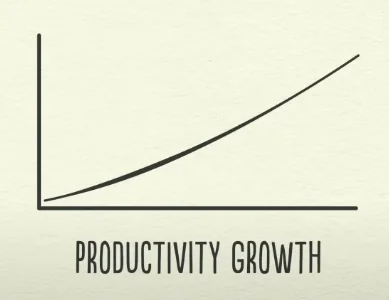

Productivity Growth

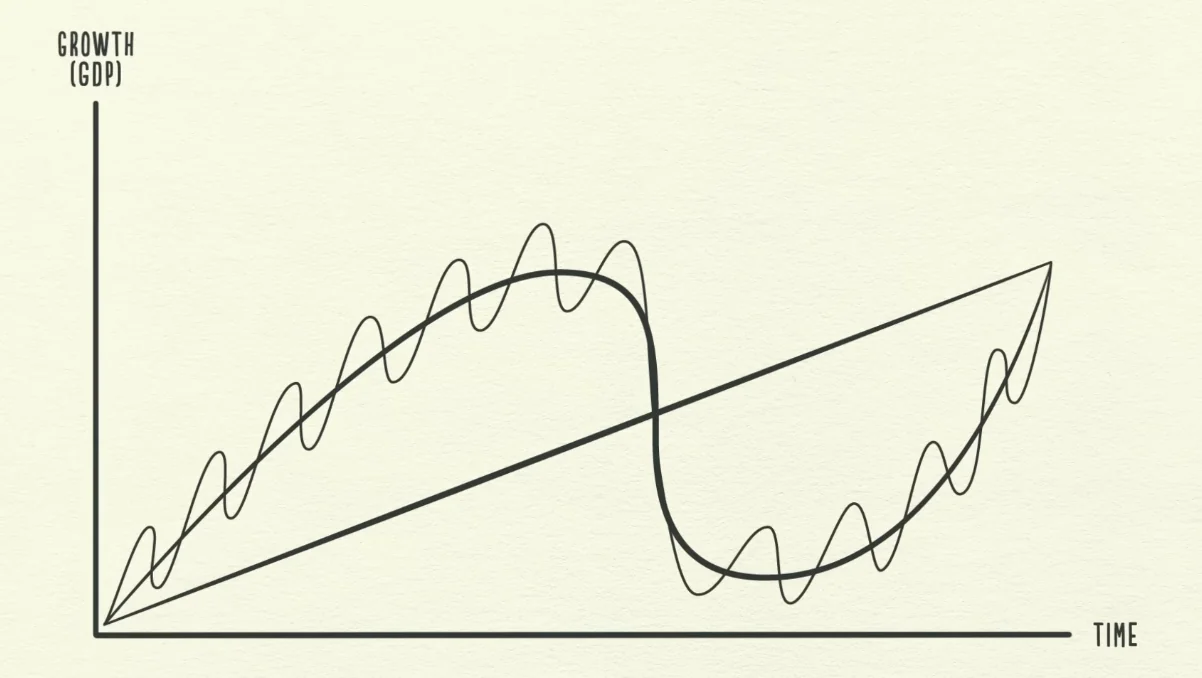

Remember, in a transaction, we get income (money) for whatever goods / services / financial assets we offer in return. The price we can put on the sold quantity depends on the quality and usefulness of the quantity. Over a period of time, humans learn, humans innovate and humans evolve. In essence, over a period of time, an experienced professional is able to do quality work in a shorter period of time. Or a startup founder who has studied the market and worked on a solution for years is able to use that experience to develop new goods that solve difficult problems. We see further by standing on the giants of yesterday. Those that are hardworking and inventive increase their productivity and living standards faster over a long period of time. Productivity growth is stable, strong, predictable and grows slowly. Because it doesn’t fluctuate much, it is not a big driver of economic swings.

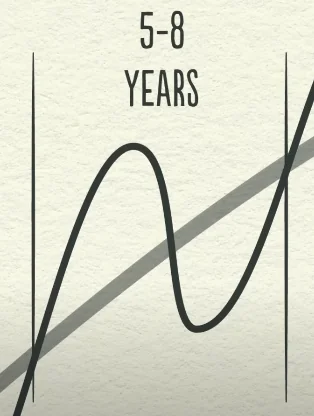

Short-Term Debt Cycle

Debt on the other hand, is far more short-term focused and occurs in cycles. When you take up debt, it allows you to consume more than you produce. And when you are paying back debt, you are forced to consume less than you produce. Debt swings, according to Dalio, occur in two big cycles. Short-term debt cycles occur $\approx 5-8$ years. These swings are primarily caused based on how much credit there is active in the economy.

Let’s see how it works. These ‘cycles’, as described by Ray, occur because of our human nature to borrow money. Borrowing money is essentially just a way to manage buying power over a period of time. To spend more than you make today, you borrow from your future self. Essentially you create a time in the future when you need to spend less than you make in order to pay it back. One reason why you would do this is to smooth-en your buying power over time. Remember that in the future, your income increases because you’re more productive and you are likely to make more money. So it makes sense to you to borrow more from your future self as you know your future self will be likely making a lot more money. And getting access to more money early is a lot more profitable because if you’re able to invest it well, you can generate a lot of money from it due to the simple POWER OF COMPOUND INTEREST.

The very act of borrowing, creates a very mechanical and predictable series of events that will happen in the future. If you borrow now, you must pay it back later. This is just as true as it for an individual, as it is for the economy as a whole. This series of events will always occur in a cycle.

Is Credit Always Good?

Not really. If you borrowed credit just to spend more on liabilities and you do not increase your productivity or income growth in any significant way, it it bad. You now create a time in the future where you need to pay back this debt with the same income level you have today. It wasn’t used to create any meaningful growth.

“If you can’t buy it twice, don’t buy it”

Super-Charging the Economy

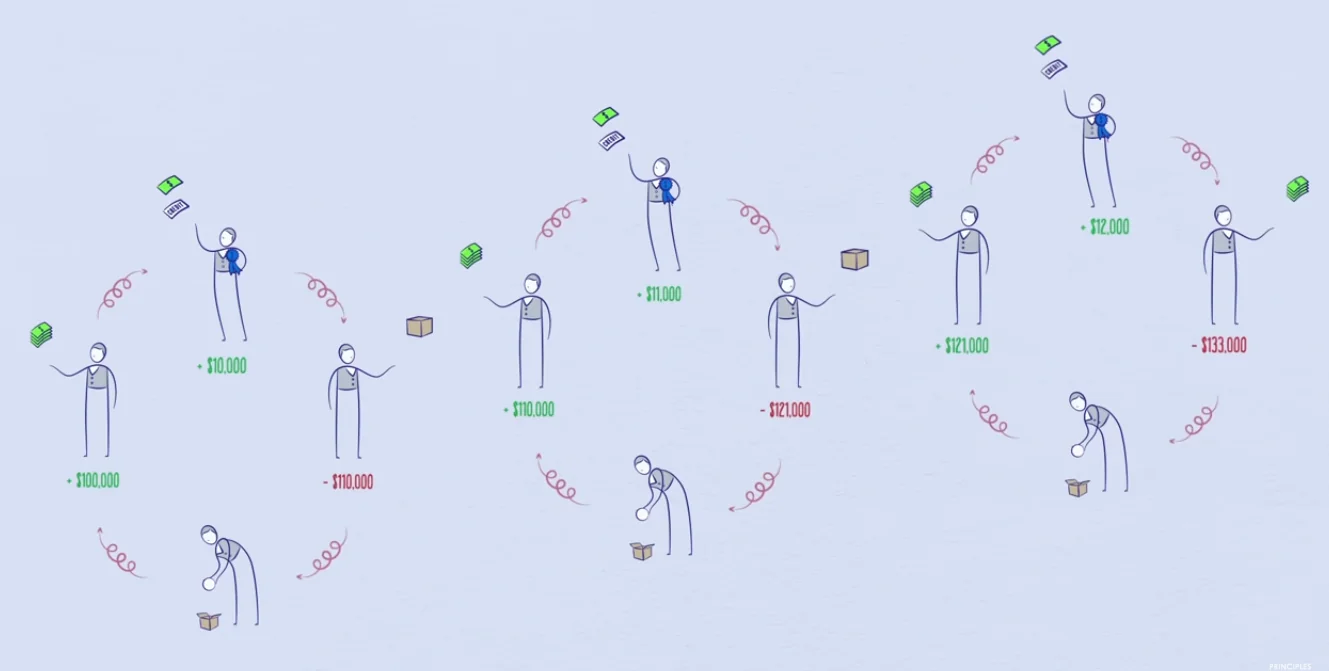

When interest rates are low, a lot of people are encouraged to borrow, and this has the effect of supercharging incomes in an economy. This is how it works, let’s say an individual $A$ earns $100,000\$$ a year and has no debt. He is credit worthy enough to borrow $10,000$$. Now, let's say he spends all his money. His spending is now $110,000$$ instead of just $100,000$$. And applying the single most important principle used to describe this whole machine, _since one person's spending is another person's income_, somebody else makes $110,000$$. This makes them credit worthy to borrow $11,000$$. Then they spend $121, 000$$ (instead of just $100,000$$), and again since their spending is somebody else’s income… this process self-reinforces itself and causes living standards and income to rise for everyone!

Since a lot of the money flowing in the economy is actually credit (money that would’ve otherwise not been involved in transactions), it encourages people to borrow since they are credit worthy to borrow more money due to their increased income (which was a result of others spending borrowed money) and become a self-reinforcing pattern. This pattern, like discussed before, will be a cycle. And if the cycle goes up, it eventually must come down.

Phase 1 - Economic Expansion

As economic activity increases, there’s an economic expansion. This is the first phase of the short-term debt cycle. People’s income rises, and spending continue to increase. However, this rise in spending is not matched with an increase in the quantity and quality of goods produced. This is because the increase in quantity / quality of goods is associated with productivity growth, and that is a much slower and stabler force than the fast-paced credit cycle. Now because we have increased spending (demand) and the supply remains the same, prices of goods go up. This is called inflation. However, the central bank doesn’t want too much inflation, because it causes problems. Seeing prices rise, it raises interest rates, launching us into the second phase of the short-term debt cycle.

Phase 2 - Economic Recession

With higher interest rates, borrowing becomes less appealing. Fewer people borrow money, and the cost of existing debts increases. This naturally causes humans to prioritize debt repayments more and borrow less. Put in this situation, the amount of money individuals have left, after paying debt repayments and not borrowing credit, is lesser than what it would’ve been in the previous phase. And since one person’s spending is another person’s income, people’s income drops. This pattern is exactly the same as we had previously during the first phase, but in the opposite direction. Incomes drop, borrowing slows and the economy falls as the money spent in transactions drops sharply. And in contrast to before, the supply remains constant but the demand drop since people spend less. This causes the price of goods to go down, we call this deflation. Economic activity decreases and we have a recession.

Flipping the Switch

Recession is clearly not good for the economy. Remember that the central bank increased interest rated on credit borrowing to help beat inflation. If they caused this to happen, they have the power to pull the economy out of a recession to. If the recession becomes too severe and inflation is no longer a problem, they can simply lower interest rates again and plunge the economy back into the first phase of the cycle.

The short-term debt cycle is primarily controlled by the central bank. When there is surplus credit flowing through the economy, there is expansion and people’s incomes and living standards rises. When there is too little credit in the economy and spending slows, there’s a recession. And it is the central bank which carefully varies interest rates on credit borrowing to keep this cycle going in a mechanical fashion. According to Ray, this cycle typically lasts 5-8 years and repeats itself over and over again for decades.

Long-Term Debt Cycle

However, in practice, we will often see that the bottom and top of each cycle finish with more growth than the previous cycle and more debt.

This occurs primarily due to human nature / greed. We as humans have an inclination to borrow and spend more instead of paying back debt. Humans push it too far. Paying back debt is boring and painful, spending more than you earn gives you more gratifying experiences. But this mountain of debt can’t keep growing forever, we eventually reach a point where debts grow faster than incomes and this creates the long-term debt cycle.

The Expansion Phase

The crazy thing is, despite borrowers debt-burdens growing, lenders even more freely extend credit. Because when living in a particular point along this curve, people focus only on what’s been happening lately. Looking at a curve from too up-close just shows you a straight line. When we are in the expansion phase of the long-term debt cycle, incomes are rising, financial asset prices are sky-rocketing, the stock market hits new peaks. Why? Because of all the credit flowing through the economy, a lot of credit is being used in transactions. Causing all the aforementioned events to occur. It’s an economic boom! When people do a lot of this, and most of it is actually using credit, we call this a bubble.

Even though debts are growing, incomes have been growing nearly as fast to offset them. And more importantly, remember the factors that make someone creditworthy? Income levels and collateral. Because financial asset prices are sky-rocketing, people have more collateral to lay down and take debts on. Note that the value of these financial assets are not fixed, and depends on the supply-and-demand for said asset in the market. And even though its increased price is mostly caused due to the artificial-demand induced due to credit in the market, most people don’t realize this as they’re looking at just what’s been happening lately.

Debt Burden

We call the ratio of debt to income the debt-burden. $DB = \frac{debt}{income}$. As long as incomes rise, the debt-burden remains manageable.

Because people own financial assets as investments that make their prices rise even higher. People feel wealthy and remain creditworthy despite being under major debt.

The Recession Phase - The Deleveraging

However, over decades, the debt-burden eventually begins to tip towards the unmanageable side. Incomes can’t rise fast enough to match the debt-repayment amounts. Just like in the recession phase of the short-term debt cycle, people cut spending. This again becomes a self-enforcing pattern like in the short-term debt cycle case. But with one crucial difference.

In a short-term debt cycle, there was a savior installed in place to flip the switch and get the economy up and growing again. The central bank could just flip the switch, lower interest-prices and allow people to borrow credit again. Increasing spending, and creating a self-reinforcing pattern that boosts the economy. However, in a deleveraging, interest prices are already at $0\%$. The central-bank cannot easily ‘flip a switch’ and fix the economy.

Debt-burdens have simply become too big. In a deleveraging, people cut spending, the stock market crashes, prices of financial assets drop as demand for them subsides, social tensions rise and the whole imaginary bubble pop, leaving behind a total shit-show. Because people’s income falls and debt repayments rise, borrowers are squeezed. They are no longer creditworthy, and borrowers cannot borrow more to payoff debts. This causes borrowers to go to their backup plan, the same backup plan the lenders trusted to give borrowers their loans. Collateral. Borrowers are forced to sell off their financial assets in order to complete their debt repayments. But this happens at a massive scale. Because the supply for financial assets suddenly soars, at the same time people cut their spending, the prices of these financial assets drop. To much lower than what it was previously, making borrowers even less credit worthy and still unable to payoff debts.

People feel poor. Less spending -> Less Income -> Less Wealth -> Less Credit -> Less Borrowing -> Less spending -> …

Lenders don’t lend more money because they are still waiting for debt repayments that they’re no longer sure if the borrower can payback and they need all their money with them to survive the deleveraging. Borrowers can’t borrow any more money and can’t pay off their existing debts. Their entire economy becomes not credit worthy.

How to Get Out of a Deleveraging?

There are 4 ways to reduce the debt burden. Some inflationary and some deflationary. They usually tend to happen in the following order:

Cut Spending (↓)

This is usually the first and instinctive reaction to most people during a deleveraging. Because the news is filled with bad news about the economy and because they realize they have a lot of debts to pay and are unable to borrow, people cut spending in order to pay off their debts. However, because one person’s spending is another person’s income, this process is deflationary in nature. Demand drops, making asset prices and incomes drop. This has the opposite effect of helping because although debts might reduce, incomes also reduce. And often incomes fall faster than debts, causing the debt-burden to grow even worse.

Debt Restructuring (↓)

The next call to action is usually debt restructuring. In this economic-crisis, many borrowers find themselves unable to pay off their debts. And remember, a borrower’s debts are a lender’s assets. When borrowers are unable to repay the bank (lender) and default, people get nervous that the bank won’t be able to repay them and rush to withdraw money from the bank. Banks get squeezed and banks default on their debts, often starting a chain of bank collapses because there is often a lot of money shared between banks.

Much of an economic-depression is people discovering much of what they thought was their wealth isn’t really there.

In such situations, lenders often agree to debt restructuring. This means lenders agree to restructure the terms of the original agreement on which the loan was taken. This could include changes where the interest is lowered, the amount to be paid back could be reduced, or the time-frame over which the debt has to be payed back could be increased. Lenders are forced to agree in these situations because the choice for them is essentially between “all of nothing” or “half of something”. This is however, still deflationary in nature because income and asset values fall as a result of debt restructuring. Money that could be injected into the system via transactions doesn’t enter because the agreement no longer requires it to.

Wealth Redistribution (↓)

The next option to help get out of a deleveraging is to redistribute wealth between the rich and the have-not. Because people’s income falls, the amount they pay in taxes falls and this directly impacts the income of the central government. At the same time the government finds itself in a situation where it needs to increase its spending because unemployment has risen due to companies laying off workers, etc. and left many people with inadequate savings to survive. This situation is called a budget deficit. A budget deficit occurs when expenditures surpass revenue and then up impacting the financial health of a country. In such a situation, especially since wealth is typically concentrated in the hands of a small percentage of the population, governments raise taxes on wealthy which allows to redistribute wealth in the economy from the rich to the have-not. This naturally increases resentment between the rich and the poor and could lead to social disorder. This sort of a situation lead to Hitler coming to power, war in Europe, and depression in the United States.

Print Money (↑)

The issue in the first place is that a lot of what people thought was their money didn’t really exist. It was credit which was borrowed from their future self. While the central bank cannot lower interest rates further, like in the case of short-term debt cycles, it still has one final card up it’s sleeve. It can print money! Unlike the aforementioned methods, printing money is inflationary. This is because the act of printing money increases the amount of money in circulation (being used in transactions), thus increasing the income of people. And because one person’s spending is another person’s income, this causes incomes to rise and asset prices to increase. However, note that the central bank cannot do this alone. Because it can only buy financial assets (which still drives up asset prices) and bonds, it focuses on buying government bonds, essentially loaning money to the central government, which then uses this money and distributes it to the poor and helps combat the budget deficit. But note that this still increases government debt.

Further, note that printing money essentially lowers the worth / purchasing power of a single note. Policy makers need to carefully balance the inflationary ways with the deflationary ways to smooth-en the debt cycle while keeping panic and social disorder at minimums. Dalio terms a deleveraging where these forces are balanced perfectly a beautiful deleveraging. In a beautiful deleveraging, debts decline relative to income, real economic growth is positive and inflation is kept under control.

This isn’t easy to balance. Printing money is an easy solution but this could lead to unacceptably high inflation by thrashing the power of a rupee / dollar / insert-currency-name-here note. Because printing money is the only method that allows incomes to rise, it must be done. The only way to reduce the debt-burden is to increase incomes in the country relative to interest rates on debt repayments so that incomes are just high enough to outgrow debt payments. When this balance is achieved, it allows the country to grow out of the deleveraging phase of the long-term debt cycle in a less-dramatic and smooth fashion.

Eventually, incomes increase, people become credit worthy and we enter the expansion phase of the long-term debt cycle again. Dalio expects the deleveraging phase to take around a decade.

Rules for Handling Macro-Economics

- Don’t have debts rise faster than income. -> Fairly obvious, debt-burdens getting out of control is why we have depression phases of cycles. If we can handle it smoothly by increasing our future self’s income (via increasing productivity), we would be dealing with a much smoother and less-dramatic entry back to the expansion phases.

- Don’t have income rise faster than productivity. -> This makes you unmotivated and non-competitive if you don’t have a reason to keep pushing yourself.

- Do all that you can to raise your productivity. -> Fairly obvious again, raising productivity is what let’s you increase income in the long run and let you handle the debt repayments caused by your past-self borrowing money from you on the trust that his future self would have much higher income and buying power.

Resources referred to: