When deciding how to invest in stocks, we all know that it’s best to “buy low and sell high”, but when is a stock price low? And when is it considered high? Are there more quantifiable ways to measure these qualitative terms? Stock multiples try to solve this problem by helping traders figure out how much you pay for a stock’s underlying business and if this price has changed over time. Essentially, a stock multiple is a ratio that compares the current stock price to some fundamental quantity of the stock’s underlying business. In general, the higher the multiple, the more expensive the stock is considered to be. The idea can be more intuitively explained via the following example:

In shopping for Pork, Beef, or Chicken it’s difficult to compare the total prices since the quantity you get is different for each cut. But if we look at the price per pound, you can easily figure out which cut is the best bang for your buck. Multiple’s work in a similar way, allowing us to compare the price of a stock to the underlying fundamentals you get with the purchase - Stock Multiples: How to Tell When a Stock is Cheap/Expensive - The Plain Bagel

PE Ratio

A PE Ratio is a stock multiple which compares a company’s current stock price to its earnings per share (EPS). It’s one of the most popularly used stock multiples and it helps assess the relative value of a company’s stock. It’s very useful when used to compare a company’s valuation against it’s historical performance, or even other firms in the industry or the entire market in general. (What is the Stock Market?)

For example, let’s say company $A$ was split into 20000 shares and each share was currently trading for ₹10 in the open market, and the company’s earnings (net income) for the previous year was say ₹10,000, then the EPS is $\frac{10000}{20000} = 0.5$. Computing the PE from this is, $PE = \frac{\text{Price}}{\text{EPS}} = \frac{10}{0.5} = 20$.

Note that in this example, we used the previous year’s earnings. But this might not be very representative of how the company will do this year. Perhaps it’s an oil company and the company has just placed several environmental restrictions on it that might restrict the profit making abilities of the company significantly. Or perhaps the company was involved in some massive scandal which caused consumers to lose faith in the company’s products. Regardless, this measure of EPS is a trailing measure. And hence this computation of the PE ratio is called as the Trailing P/E. However, it is also possible for analysts to try to estimate the earnings of the business for the current financial year using publicly available data and compute a new PE using these expected earnings per share. It is then called the Forward P/E. While forward P/E can escape the traps that trailing P/E is susceptible to, it has it’s own drawbacks. The primary one being that expected EPS is, as the name says, expected. These estimations may not pan out and then we would have some unexpected error margin to deal with.

Now, let’s say we have decided to use one of the P/E measures and compute the value to be $x$. What can we infer about a stock’s price based on this value? Using just $x$, we can’t say much. This is because P/E is a relative measure. It does not make sense by itself. But we can compare the stock’s current P/E to it’s historical P/E values, or even with the stocks of other companies in the same sector.

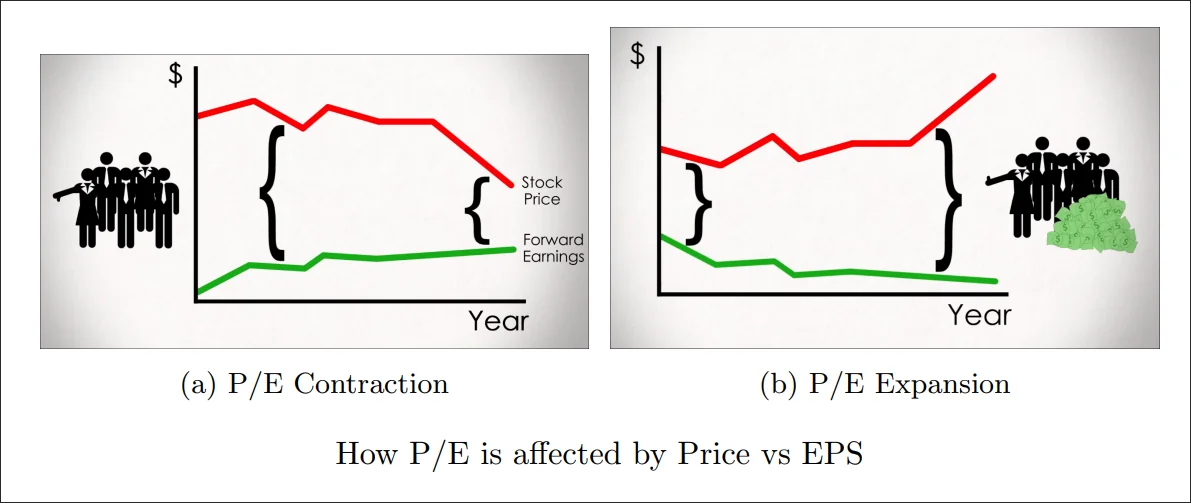

Historical Comparison

If the company’s earnings are expected to increase, but the price of the stock has fallen, it would mean that the multiple has contracted, and investors don’t value the profitability of the firm as much as they used to. Alternatively, if earnings are falling but the price has risen, the multiple has expanded, meaning people are paying more for less profit. We could also compare the P/E multiple to the stock’s long-term average to see whether the margin is larger or smaller than normal. If the stock’s ten-year average P/E is 15 times, for example, we can assume that the stock’s multiple is temporarily cheaper than normal and may want to buy if we pick up the stock in the multiple later expands back to its long-term average. Then we could earn a return even if the company’s earnings are flat. A key assumption here is that a multiple is expected to revert to its mean over time, and while that doesn’t always hold true, investors sometimes look for extreme variations from the mean, with many believing that short-term volatility in the stock, which could be caused by a bad press release or negative near-term headwind, will eventually subside, causing the multiple to return to its normal level. - Stock Multiples: How to Tell When a Stock is Cheap/Expensive - The Plain Bagel

Industry Comparison

Comparison of the multiple w.r.t to it’s historical performance is useful, but it’s important to compare it against other companies in the industry as well. Of course, a company might have higher P/E than it’s peers simply due to having a better culture, better marketing team, etc. but it’s still useful when comparing two companies to directly compare how two companies are valued against each other simply due to the fact that the underlying product they are selling remains the same. If a stock $A$ has higher multiple than stock $B$, where both the underlying companies only sell footballs, it does not immediately imply that company $A$’s stock is worse bang for your buck. P/Es are limited in the information that they are able to capture. Company $A$ might be growing at a much faster pace than company $B$, or it might have the necessary comparative advantage to quickly explore and capture market share in other industries, say football pumps or soccer shoes. This is why stocks in the tech space usually have higher multiples than their peers since they tend to have high growth potential.

A multiple contraction might imply that it is trading at a lower price than it’s supposed to, and might signal a potential buying opportunity, but it could also be a value trap. A value trap is where an investor buys a cheaper lower-quality item just because it’s cheaper. Sometimes the contraction could be justified, and in other situations it might signal a good buying opportunity. It is therefore important to use stock multiples along with a strong understanding of the fundamentals of the company to decide which of the two we as an investor believe the contraction to be a result of. Multiples are a very handy way to quickly understand a stock’s price values. Some investors even contest that the P/E ratio in particular is very limited since EPS can easily be manipulated by accounting decisions and manipulation.

“It’s far better to buy a wonderful company at a fair price… than a fair company at a wonderful price.” - Warren Buffet